As someone who enjoys studying market data, I find the months that require the most interpretation are often the most interesting.

May is one of those months.

At first glance, the numbers may appear softer than those reported earlier in the spring. New listings increased, while under contract activity, closed sales, and median pricing all moved lower compared to the same period last year. However, before drawing broad conclusions, it is worth taking a closer look at what is driving those changes.

What I continue to see in the field is a market that remains highly selective rather than broadly weak. Well-priced and well-presented properties are still attracting significant interest and, in many cases, multiple offers. At the same time, buyers appear more willing to pause on properties that are perceived as overpriced, poorly positioned, or requiring substantial work.

Off-market activity also remains present across several price points, including at the higher end. Because those transactions are not reflected in BrightMLS data, the publicly reported figures do not fully capture the scope of market activity currently underway.

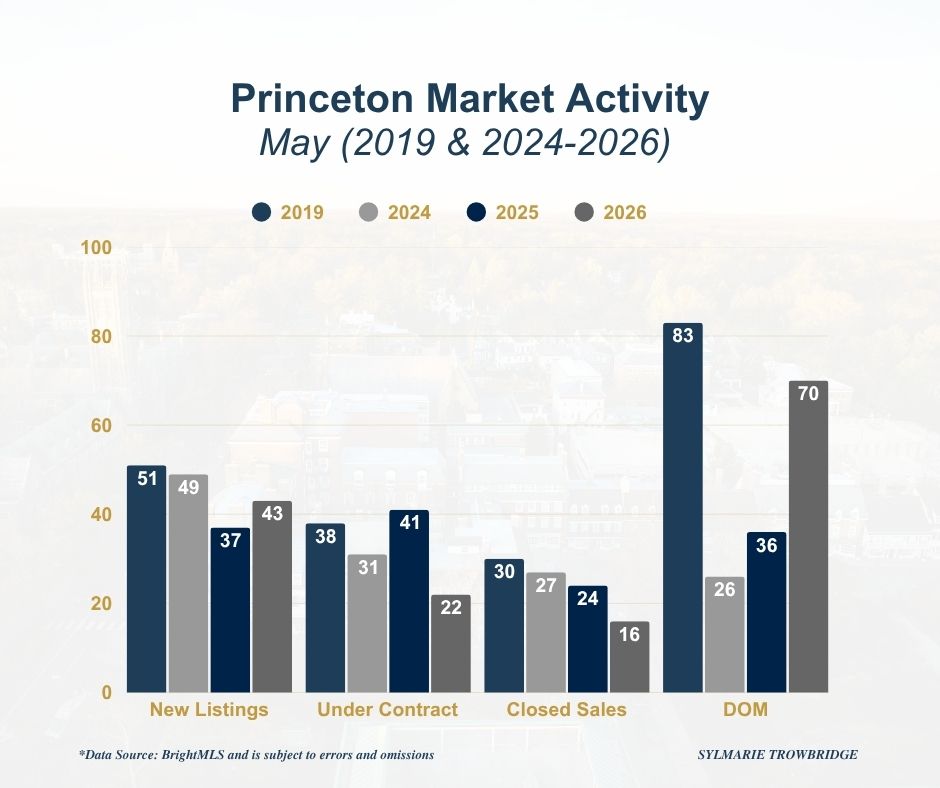

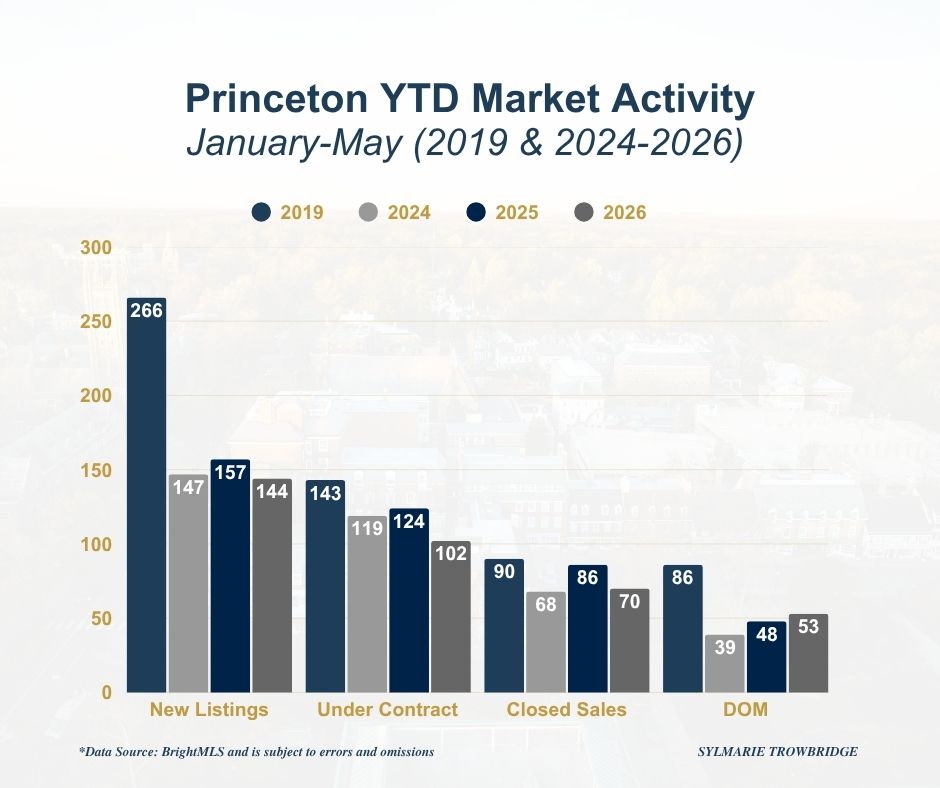

As a quick reminder, and in the spirit of continuous improvement, I continue to use 2019 as a pre-pandemic baseline alongside the most recent three years of data. I believe this provides a clearer perspective on how dramatically the market has evolved.

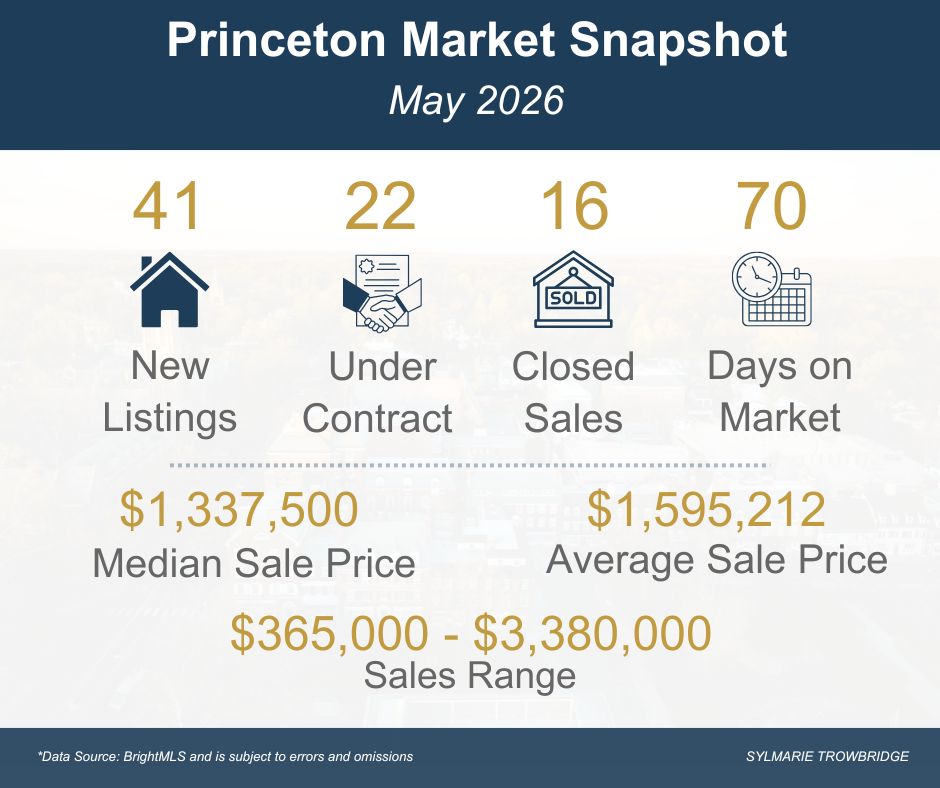

May brought 43 new listings to the Princeton market, a 16% increase compared to May 2025. However, 22 properties went under contract, compared to 41 during the same month last year. There were 16 closed sales during the month, with a median sale price of $1,337,500 and an average sale price of $1,595,212. Sale prices ranged from $365,000 to $3,380,000.

Before interpreting these figures too broadly, it is important to understand what may be driving them. While under contract activity, closed sales, and median pricing all moved lower compared to last year, the underlying story is more nuanced than the headline numbers alone suggest.

One of the more interesting developments in May was the increase in new inventory. While listings remained below both 2019 and 2024 levels, more homes came to market than during the same period last year. At the same time, under contract activity and closed sales moved lower, while average days on market increased.

Taken together, these figures suggest a market that is becoming more selective. Buyers appear willing to compete for properties that are priced and presented appropriately, but they are taking more time to evaluate homes that miss the mark. While this is a different dynamic than we experienced in 2024 and 2025, it remains considerably stronger than pre-pandemic conditions.

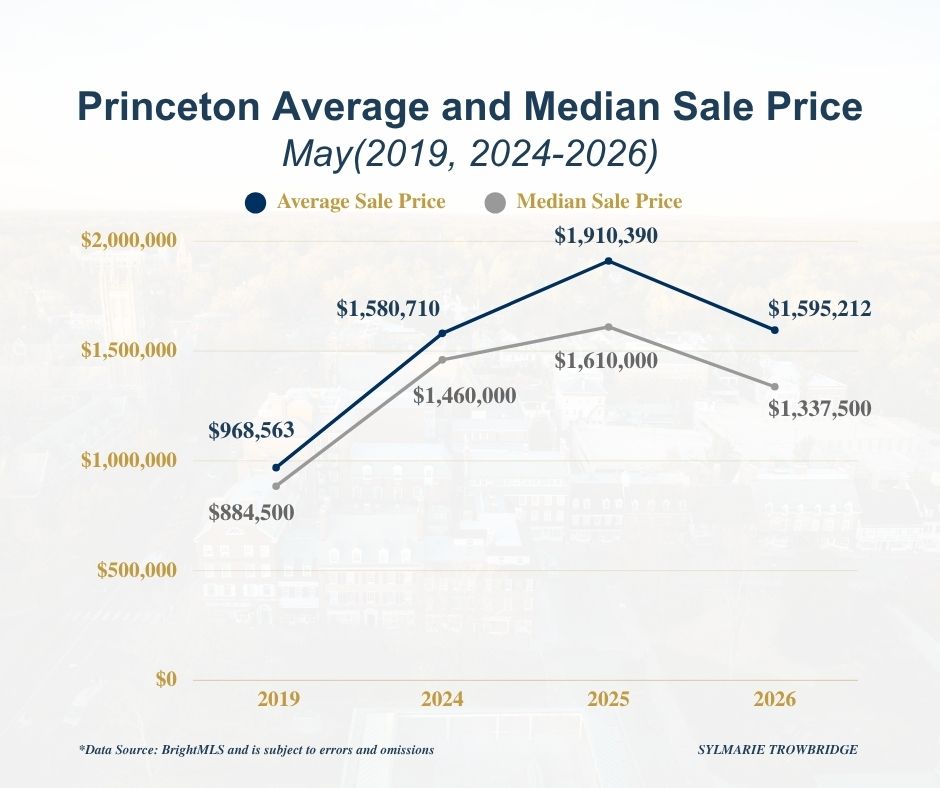

The May pricing data provides a good example of why it is important to look beyond a single statistic. Although the median sale price declined compared to last year, the average sale price was essentially unchanged. Combined with the continued presence of off-market transactions, particularly at higher price points, the reported figures likely understate portions of the market that continue to experience strong demand.

At the same time, pricing has become increasingly segmented. Buyers are responding more cautiously to aspirational pricing or properties requiring substantial updates.

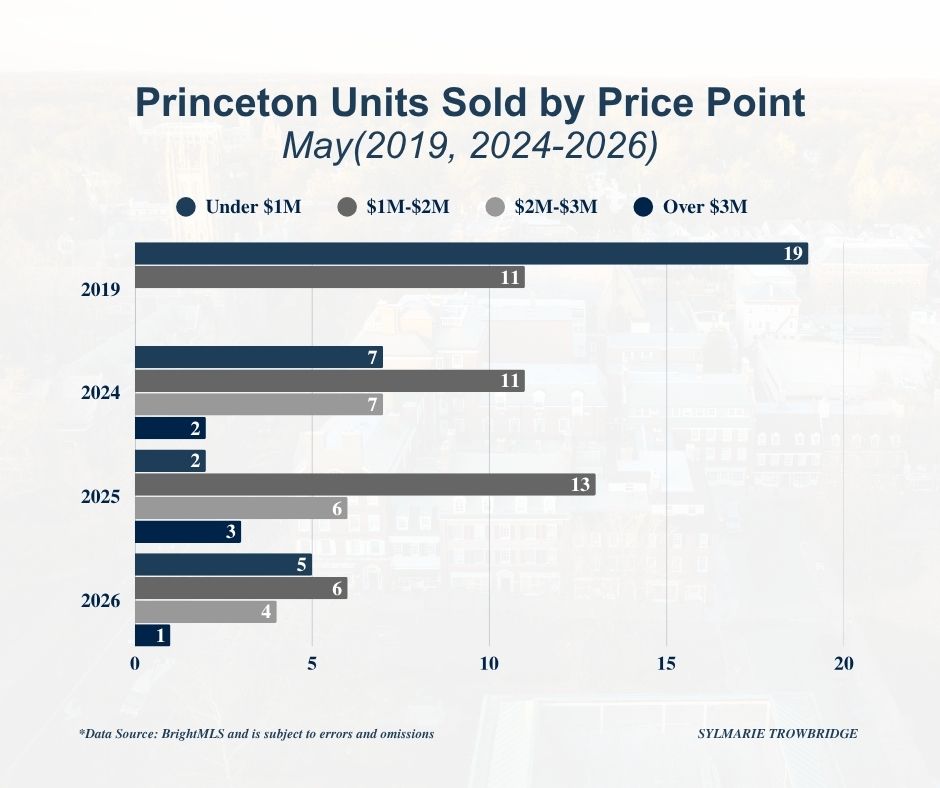

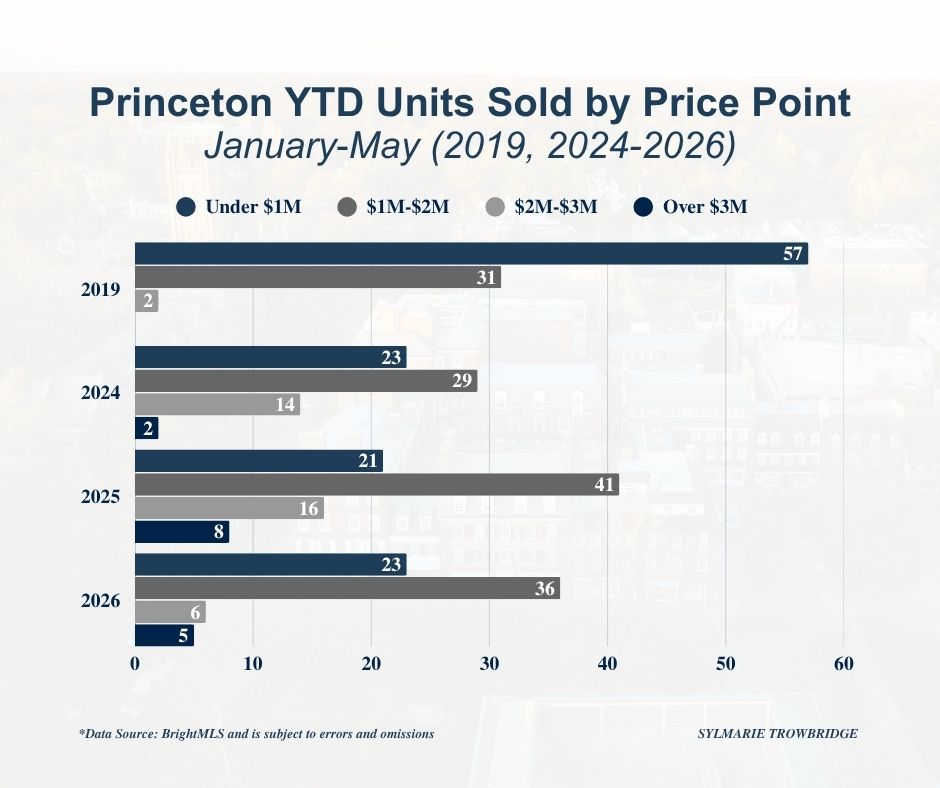

The composition of sales by price point reinforces this observation. Compared with last year, fewer transactions occurred above $3 million, while activity remained concentrated in the $1 million to $2 million segment of the market. In addition, a number of higher-end transactions continue to occur outside the MLS, further influencing the reported figures.

When viewed against 2019, today’s market remains remarkably resilient. New listings remain below pre-pandemic levels, yet pricing remains substantially higher and homes sell faster than they did before 2020.

Year-to-Date Trends

The year-to-date data reinforces many of the same themes.

Through the first five months of 2026:

• New listings declined from 157 to 144 compared with the same period last year

• Under contract activity declined from 124 to 102

• Closed sales declined from 86 to 70

While all three measures are tracking below last year’s pace, the declines are far less dramatic than the May snapshot alone would suggest.

Viewed in isolation, those figures may suggest slowing activity. However, inventory remains the defining constraint rather than a lack of buyer interest. I also wonder whether we are experiencing a later spring market this year. The winter was longer and harsher than recent years, and it would not surprise me if some buyers and sellers delayed their plans as a result.

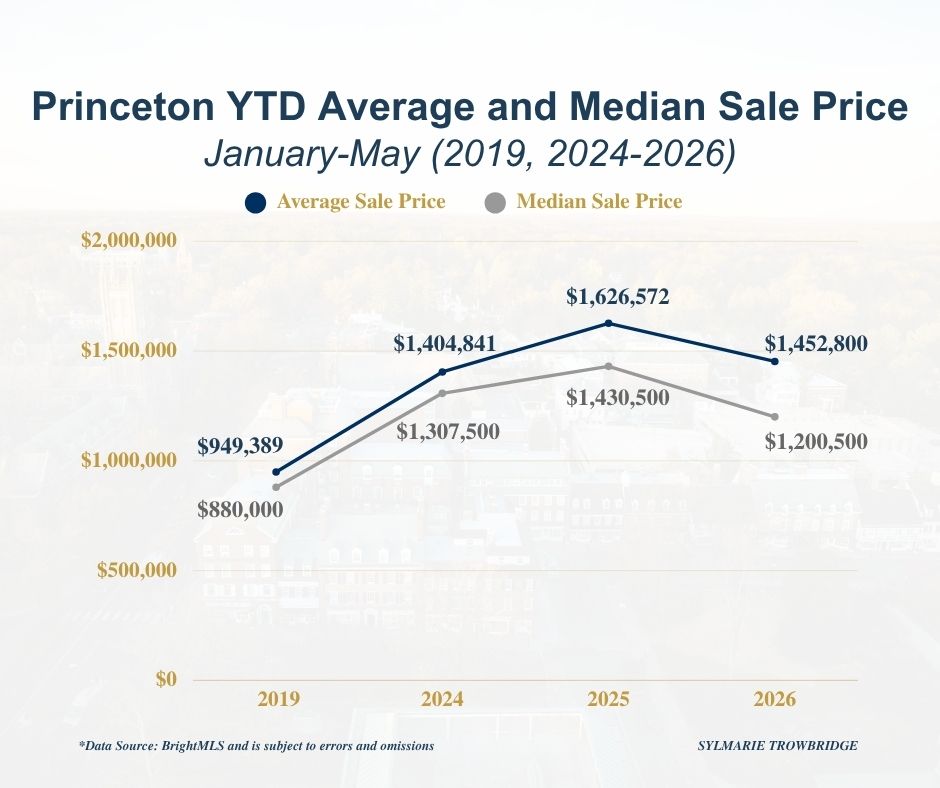

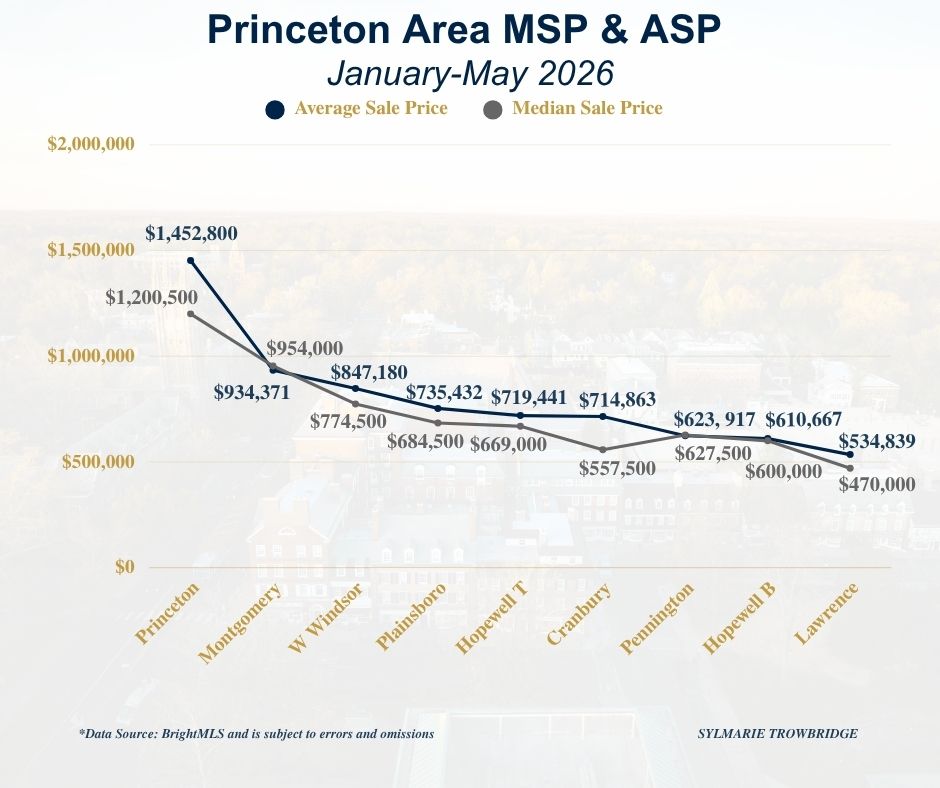

The pricing data also requires a bit more interpretation beneath the surface. Year-to-date, the average sale price stands at $1,452,800 and the median sale price at $1,200,500. While both figures are lower than last year’s exceptionally strong results, they remain substantially above pre-pandemic levels.

Part of the year-over-year difference reflects the mix of properties sold. Last year’s figures included more upper-end transactions reported through BrightMLS, while this year a meaningful amount of luxury activity has occurred off market. Because those transactions are not reflected in the publicly reported data, the year-to-date pricing figures likely underrepresent portions of the market, particularly at the higher end.

Perhaps the most important takeaway is this: despite fewer listings entering the market and fewer completed transactions, well-priced homes continue to attract buyers, and multiple-offer situations remain common for properties that align with buyer expectations on price, condition, and presentation.

What This Means

For Buyers

The increase in inventory is creating more opportunities than buyers experienced earlier in the year. While desirable properties continue to attract competition, buyers are finding more choices and, in some cases, additional time to make thoughtful decisions.

That said, the market remains highly selective. Well-priced and well-presented homes continue to generate significant interest, while buyers may find greater negotiating opportunities with properties that have been on the market longer or require updates.

For Sellers

Inventory has improved, but remains limited by historical standards. Buyers continue to engage with homes that are priced appropriately and presented thoughtfully. Multiple-offer situations are still occurring, but today’s buyers are increasingly discerning.

Condition, presentation, and pricing strategy matter more than ever. Sellers who align with buyer expectations from the outset are best positioned to generate early interest and achieve strong outcomes.

Looking Ahead

The market appears to be finding a more balanced relationship between buyers and sellers. Competition has not disappeared, but buyers are becoming more selective and sellers are facing a market that rewards preparation and thoughtful pricing.

As additional inventory comes to market, buyers may gain more options while demand continues to be supported by the area’s enduring appeal. In a market like this, my role is to help clients move beyond the headlines and understand what the data is actually saying.

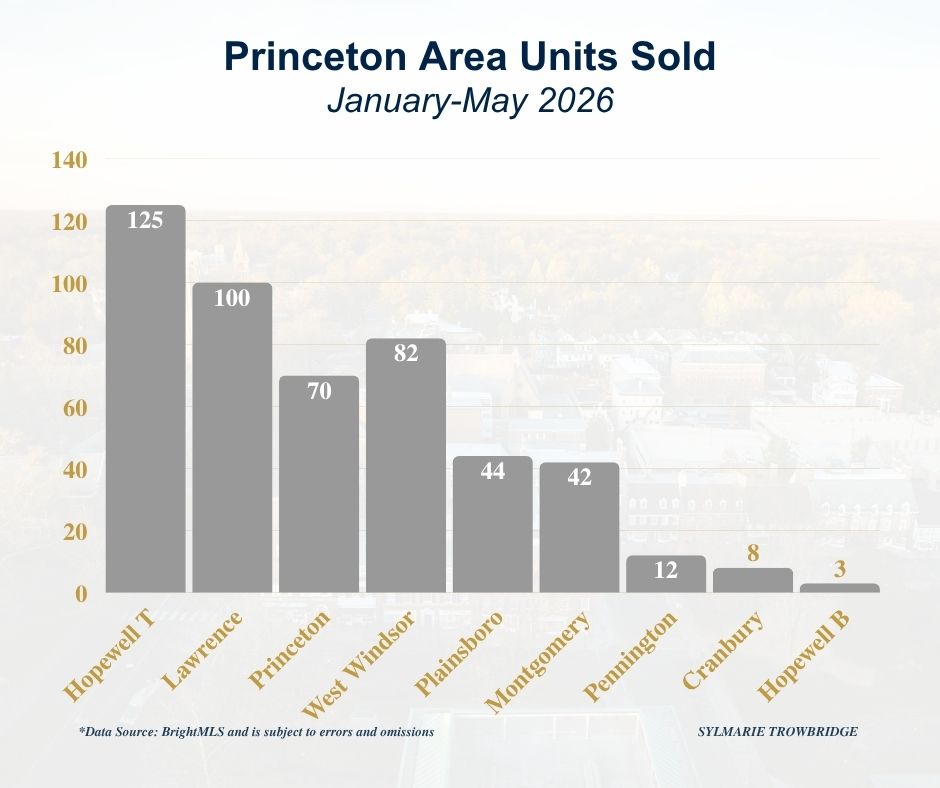

Princeton Area Overview

The broader Princeton-area market continues to exhibit varying dynamics across towns and price points. Hopewell Township leads the region in units sold, followed by Lawrence and West Windsor. Princeton commands the highest average and median sale prices, reinforcing its position as the premium pricing market within the region.

Final Thought

While some of May’s headline numbers appear softer than earlier in the spring, the underlying story remains consistent. Inventory remains limited, demand remains present, and buyers continue to compete for homes that are priced and positioned appropriately.

As always, if you are thinking about buying, selling, or would simply like to better understand the Princeton area real estate market, please feel free to call (917-386-5880), text, or email me.I am always happy to be a resource!