As the spring market continues to unfold, April provided a clearer indication of the underlying strength of buyer demand in the Princeton market. While broader headlines may suggest moderation, locally, the relationship between supply and demand tells a more nuanced story.

Most notably, buyer activity accelerated considerably despite constrained inventory levels. At the same time, off-market activity continues across several price points, including at the higher end. Because these transactions are not reflected in BrightMLS data, the reported figures do not fully capture the scope of market activity underway.

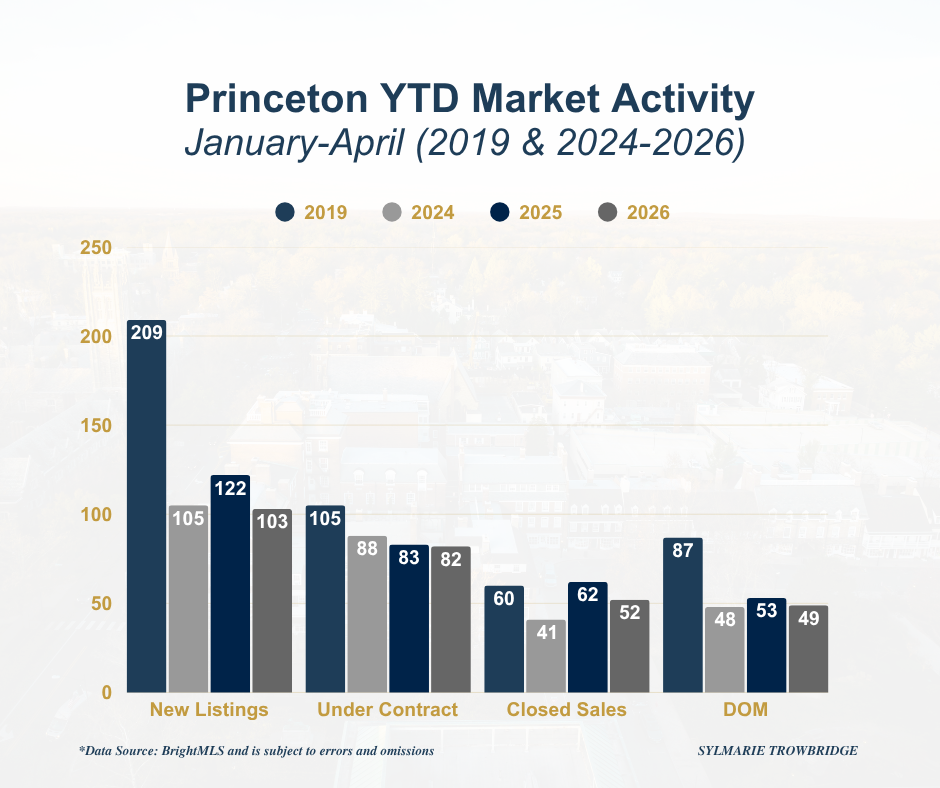

As a quick reminder, and in the spirit of continuous improvement, I continue to use 2019 as a pre-pandemic baseline alongside the most recent three years of data. I believe this provides a clearer perspective on how dramatically the market has evolved.

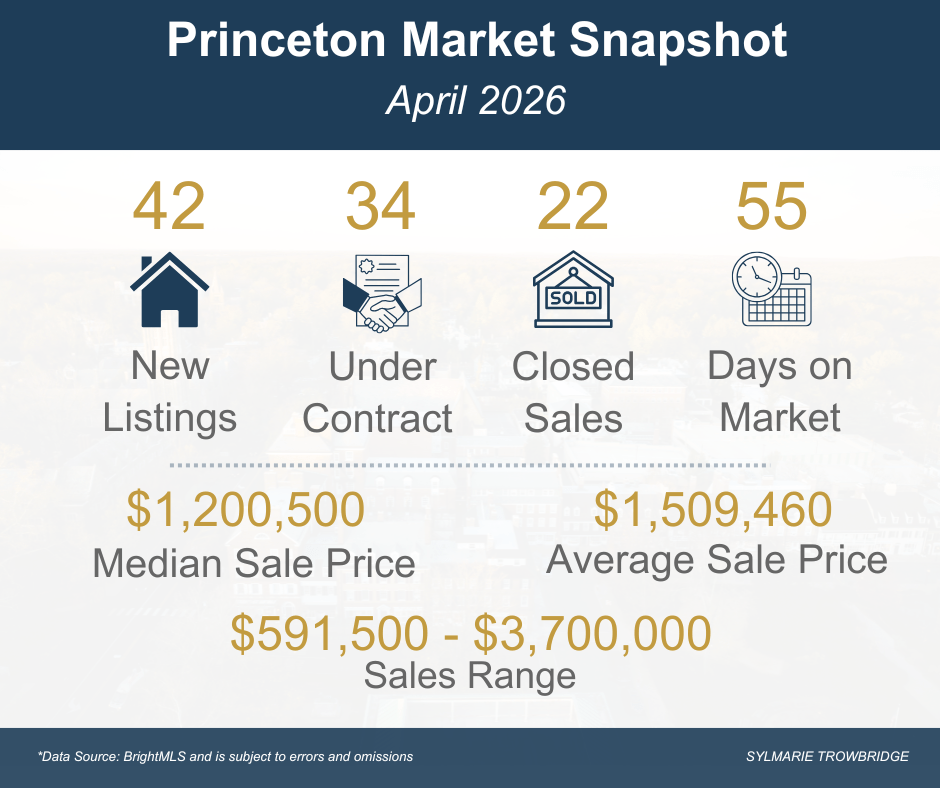

April brought 42 new listings to the Princeton market, the exact number introduced in April 2025. However, buyer engagement increased substantially, with 34 properties going under contract, a 36% year-over-year increase. There were 22 closed sales during the month, with a median sale price of $1,200,500 and an average sale price of $1,509,460. Sale prices ranged from $591,500 to $3,700,000.

At first glance, the closed sales data may appear somewhat mixed. Closed sales declined year-over-year, and average days on market increased modestly from 46 to 55. However, the increase in under contract activity, combined with relatively stable pricing, suggests buyer demand strengthened as spring inventory emerged. This distinction is important because contracts are often a leading indicator of market activity, while closed sales typically reflect purchasing decisions made weeks or months earlier.

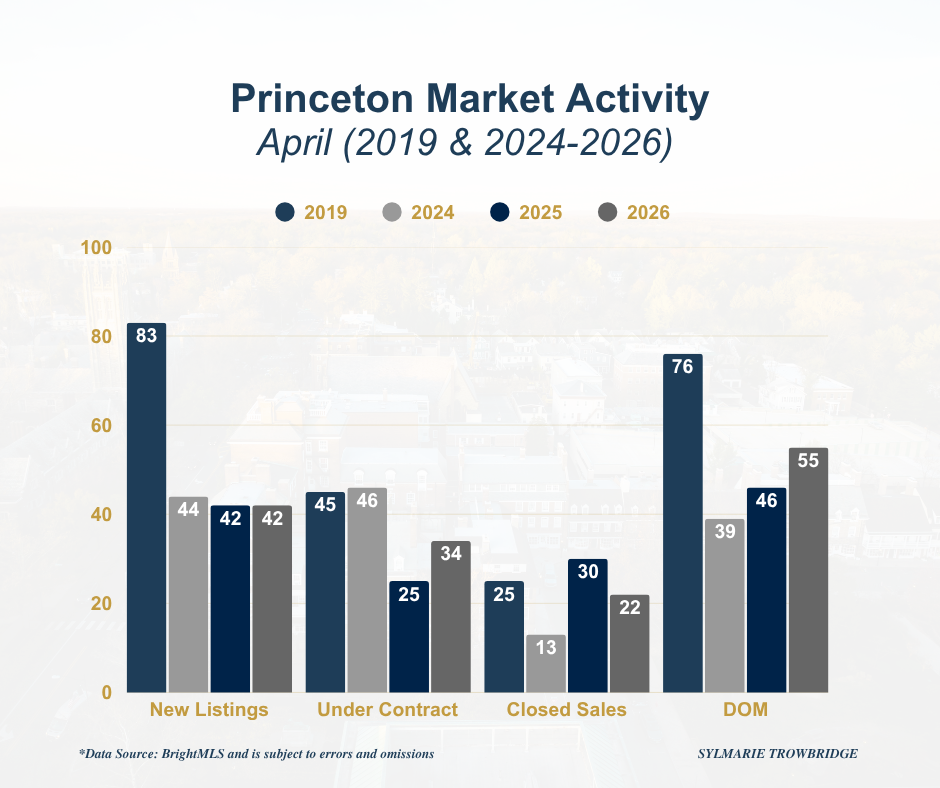

One of the most striking trends continues to be the relationship between inventory and market efficiency. Compared with April 2019, new listings remain materially lower, yet the market is maintaining relatively strong absorption levels and substantially faster transaction timelines. Average days on market in April 2019 stood at 76 days, compared with 55 days this April.

In many ways, the post-pandemic Princeton market has become extraordinarily efficient, functioning with meaningfully less inventory while still sustaining healthy buyer engagement. At the same time, the market is becoming increasingly selective. Well-priced and thoughtfully positioned homes continue to attract strong interest and, in many cases, multiple offers, while aspirational pricing is receiving a more measured response from buyers.

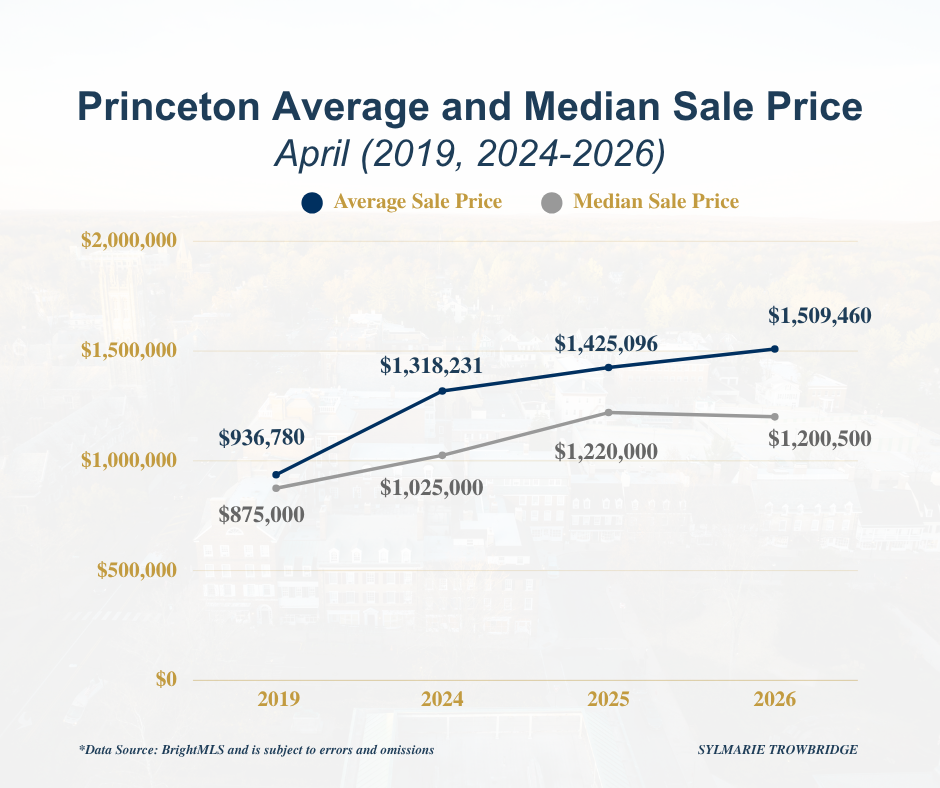

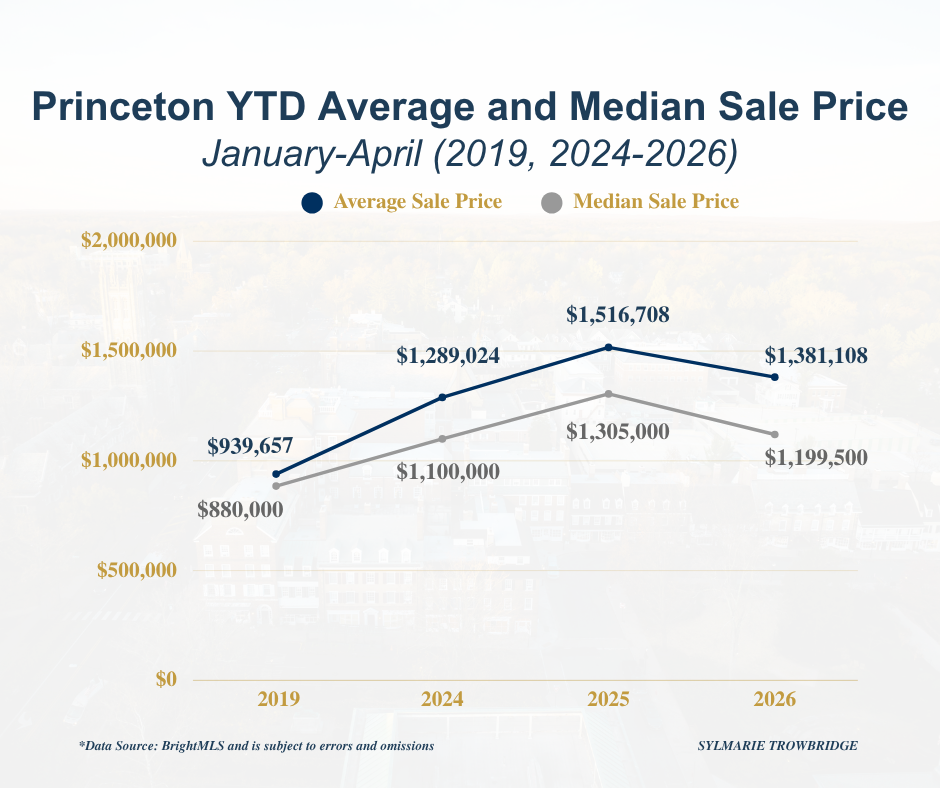

While month-to-month pricing can fluctuate based on the mix of properties sold, the broader trend continues to reflect a market that has strengthened meaningfully over time. Even with ongoing inventory constraints and a notable amount of off-market activity not reflected in the reported data, both average and median sale prices remain substantially above pre-pandemic levels.

Pricing has become increasingly segmented, and well-positioned homes are still commanding strong interest, while buyers have become more disciplined in their approach to properties perceived as overpriced or requiring substantial work.

Year-to-Date Trends

The year-to-date data reinforces many of the same themes. Through the first four months of 2026, new listings declined from 122 to 103 compared with the same period last year. While under contract activity remained nearly unchanged, slipping only slightly from 83 to 82, and closed sales declined from 62 to 52. Taken together, these figures suggest buyer demand has remained remarkably resilient despite materially lower inventory levels.

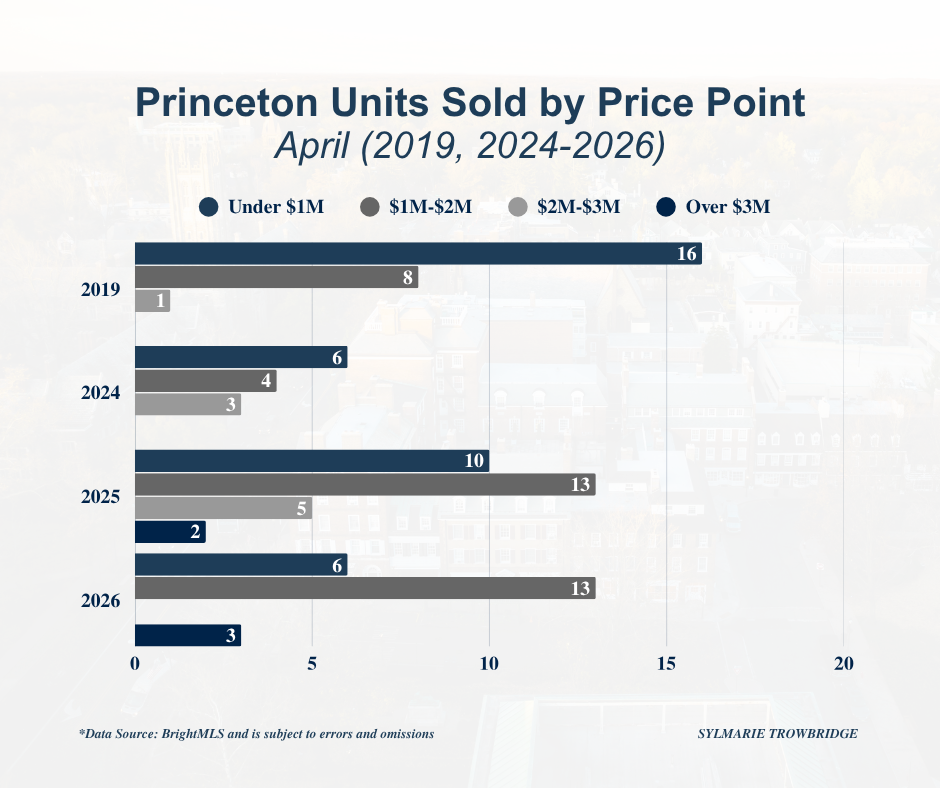

The pricing data also requires a bit more interpretation beneath the surface. Both average and median sale prices have moderated year-over-year; however, the decline appears driven less by weakening demand and more by differences in sales composition and reporting visibility.

Last year’s figures included more upper-end transactions reported through BrightMLS, while this year, a meaningful amount of luxury activity has occurred off-market. Because those transactions are not reflected in the reported data, the year-to-date pricing figures are likely to underrepresent portions of the market, particularly at the higher end.

Average days on market remain historically low relative to pre-pandemic norms, reinforcing that demand continues to outpace available supply in many segments of the market. Perhaps the most important takeaway is that despite significantly fewer listings entering the market, buyer engagement has remained remarkably steady. Inventory remains the defining constraint, not a lack of buyer interest.

What This Means

For Buyers

While inventory remains limited, opportunities do exist. Buyers who are prepared, decisive, and willing to remain flexible on condition or location are still finding success. At the same time, well-positioned homes continue to attract significant competition, particularly in the most active price segments below $2M.

For Sellers

The current market remains favorable to sellers, particularly those who approach it strategically from the outset. Demand continues to exceed supply across many market segments, but buyers are also becoming increasingly disciplined. As a result, proper pricing, thoughtful presentation, and strategic positioning matter more than ever. While broad market exposure often produces the strongest outcomes, every seller’s goals are different, and I continue to work closely with my clients to determine the approach best aligned with their priorities.

Looking Ahead

Rather than a weakened spring market, April suggests we may simply be experiencing a later and more supply-constrained spring cycle.

If inventory begins to build further in the coming months, buyers may gain additional options while competition remains supported by underlying demand. Continued off-market activity and limited supply may still obscure some of the market’s underlying strength within the BrightMLS reported data.

In markets like this, my role is to help clients move beyond the headlines by providing thoughtful interpretation, strategic guidance, and a clear understanding of how shifting market conditions affect their individual goals.

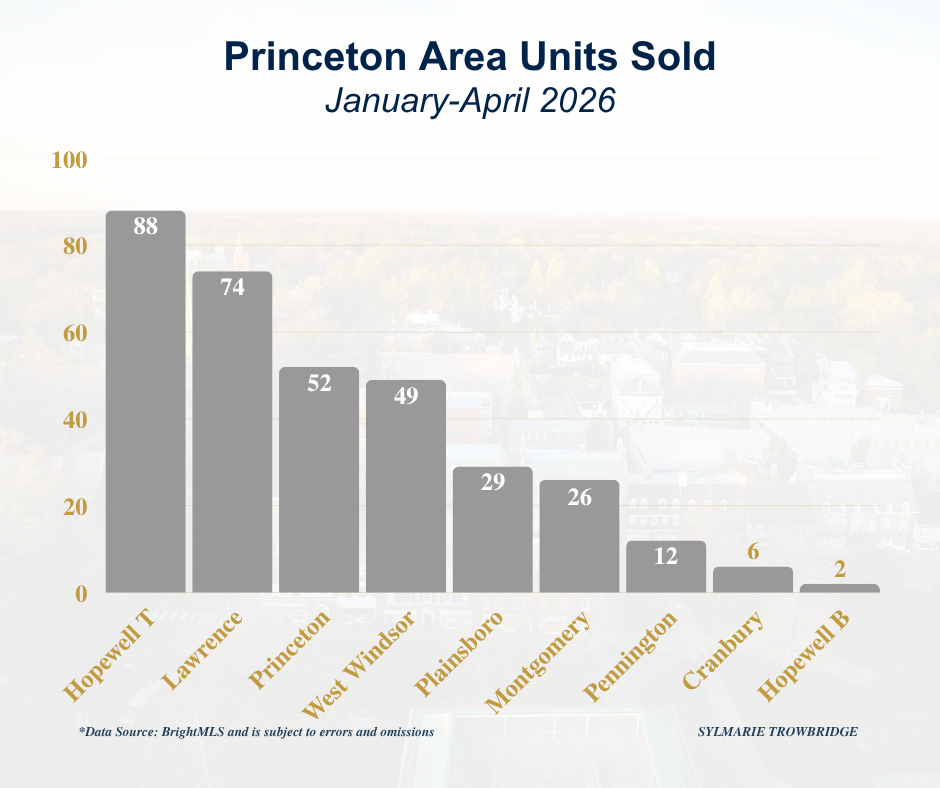

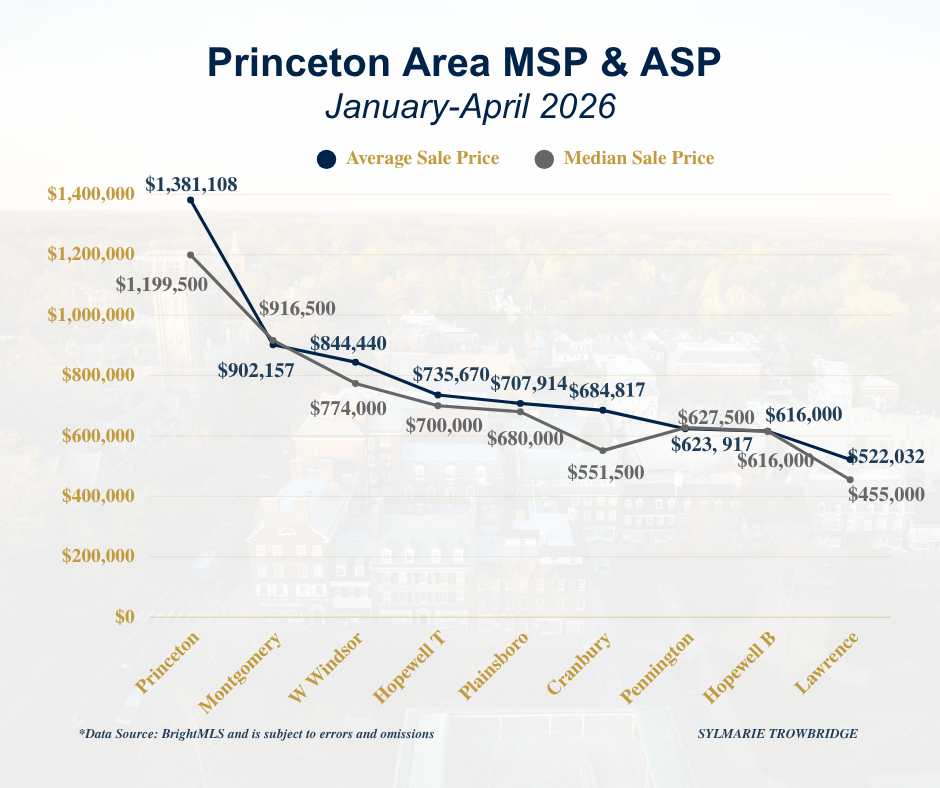

Princeton Area Overview

The broader Princeton-area market continues to reflect varying dynamics across price points and locations. Princeton remains the premium pricing market within the region by a meaningful margin, while towns such as Hopewell and Lawrence continue to experience strong transaction activity, likely reflecting buyers expanding geographically in response to inventory limitations and affordability considerations. Meanwhile, markets such as Montgomery and West Windsor continue to demonstrate resilience driven by historically strong school and lifestyle demand.

Final Thought

While monthly figures naturally fluctuate, the broader story remains remarkably consistent: buyer demand persists, inventory remains constrained, and thoughtful strategy continues to drive strong outcomes.

As always, if you are thinking about buying, selling, or would simply like to better understand the Princeton area real estate market, please feel free to call (917-386-5880), text, or email me.I am always happy to be a resource!