Much like January 2023, the February 2023 sales data continues to show that we are in a transitioning market and that we need new inventory. As you will see, the statistics we are about to share look a bit wonky and we can’t help but wonder where we would be if there was more inventory to sell.

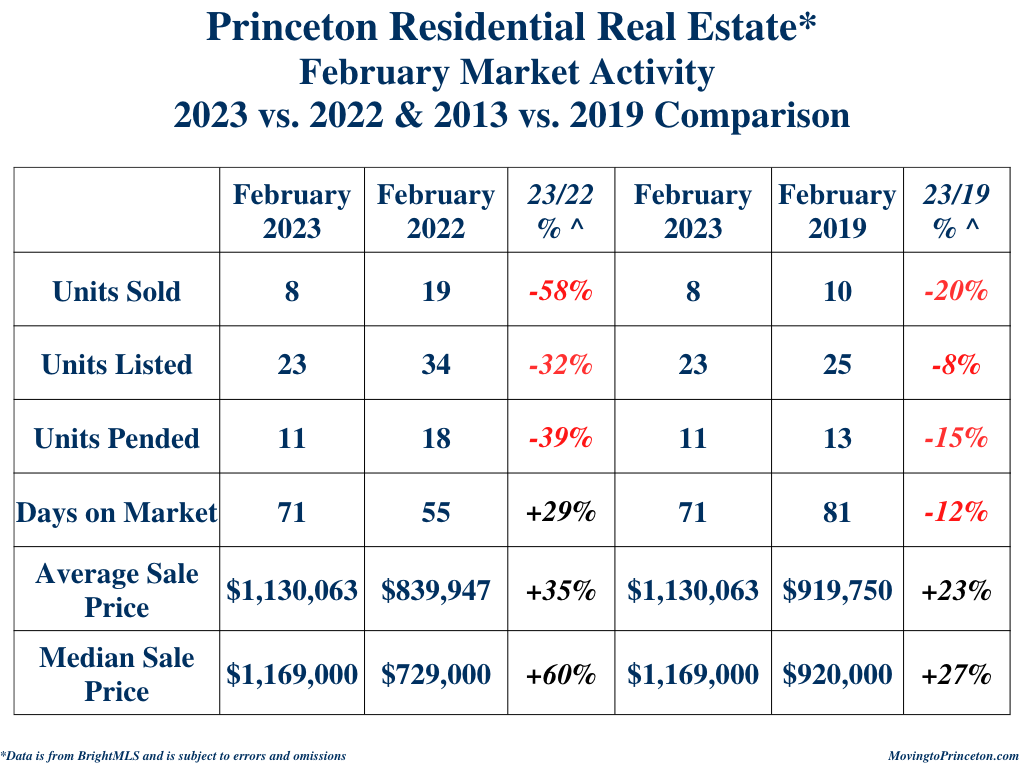

So what happened in February? There were material decreases in Units Sold (-58%), Units Pended (-39%), and Units Listed (-32%), while the Days on Market (+29%), Average Sale Price (+35%), and Median Sale Price (+60%) all significantly increased in February 2023 compared to February 2022. In other words, there were fewer new listings, fewer houses sold, and fewer properties to go under contract, but the houses that did trade sold slower and at a higher price compared to the same period last year.

Now let’s look at February 2023 versus February 2019. In February 2023, there was a 2 unit decrease across the board (Units Sold, Unites Listed, and Units Pended) compared to February 2019, and properties sold faster (-12% in DOM) and at a higher price (+23%). Curious about the years in-between? The bar chart below shares Units Sold, Units Listed, Units Pended, and the Days on Market over the last 5 years. As you will see, the market appears to be normalizing and returning to pre-pandemic levels.

The February 2023 Average Sale Price (ASP) and Median Sale Price (MSP) were also pretty extraordinary when compared to February 2022. Let’s dive a little deeper into the data to find out why there was such a difference. In February 2023 the highest sale was $2,250,000 versus $1,650,000 in February 2022. Additionally, there was a higher penetration of sales (50% vs. 11%) in the $1M-$2M price range in February 2023 compared to February 2022, when 89% of the sales were below $1M. Given the aforementioned information, it’s not surprising that there was a such remarkable year-over-year increase in both the ASP (+35%) and the MSP (+60%).

How is Princeton performing year-to-date (YTD)? Units Sold (-57%), Units Listed (-12%), and DOM (-8%) all decreased compared to January-February 2022. As for January-February 2023 versus January-February 2019, there was only a 2 unit decrease (-10%) in Units Sold but a 19 unit decrease (-30%) in Units Listed and a -39% decrease in DOM.

As for the ASP and MSP, the January-February 2023 ASP (+29%) and MSP (+34%) increased compared to January-February 2022. Relative to January-February 2019, the January-February 2023 ASP and MSP both increased +42%.

So what does this all mean? We are now starting to return to pre-pandemic levels of Units Sold, but are well below the number of Units Listed in previous years. Additionally, while we are still seeing properties sell fairly quickly, opportunities for buyers are starting to emerge.

So what is happening now? There are currently 48 Active Units between $600,000 and $4,500,000, 13 Active Under Contract Units between $600,000 and $12,000,000, and 17 Pending Units between $340,000 and $2,600,000 in Princeton. Lastly, 8 properties were introduced thus far in March between $840,000 and $3,288,000.

If you have been thinking about selling your house but have been on the fence, now may be the time to list. There are buyers – both local and out-of-town – looking to purchase a home and it would be an honor to provide you with a competitive market analysis for your property.

As always, if you are thinking about buying or selling your home or want to learn more about Princeton area real estate market statistics, feel free to email us! Sig & Syl